By Crowthorne Insurance on Dec 16, 2025 10:00:00 AM

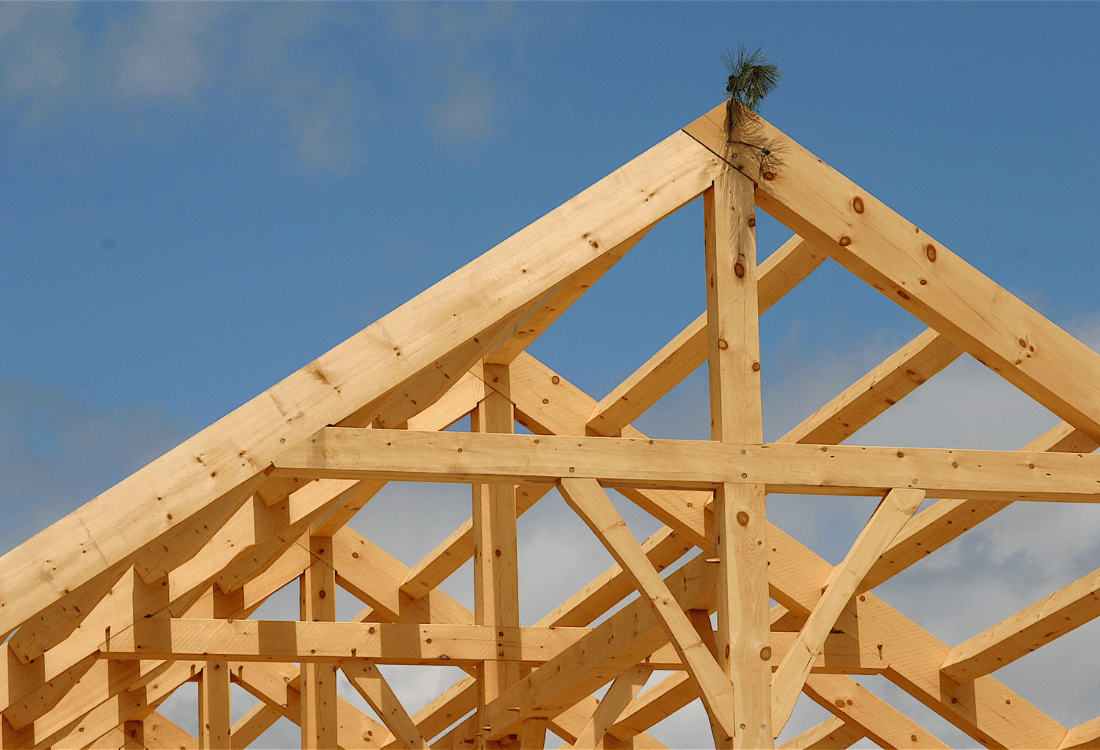

Timber frame homes have become increasingly popular in the UK thanks to their sustainability, energy efficiency, and aesthetic potential when left visible. Yet homeowners are often surprised to find that insuring these properties can be more complicated than they expected. The reason lies in how insurers classify the construction.

This short guide explains why insurance for timber-framed houses is often considered non-standard, why premiums may be higher, and how to find the right cover at a fair price.

Why Timber Frame Houses Are Classed As Non-Standard Construction

Most UK home insurance policies are based on properties built from brick or stone with tile or slate roofs. Anything that differs from this, including timber frame, is classed as “non-standard construction.”

Timber structures perform differently under certain conditions, particularly when exposed to heat or moisture. While modern timber frames are designed to meet today's safety standards, insurers often view them as a higher risk for fire and water damage.

This can make finding cover more difficult and may result in higher premiums.

Are Timber Frame Houses More Expensive To Insure?

In many cases, yes. Timber-framed house insurance can cost more than standard home insurance, though the difference depends on several factors.

Insurers price policies based on perceived risk and rebuild cost, and timber properties can increase both of these metrics.

The main considerations include:

- Fire risk: Timber is flammable, so insurers may rate it as more vulnerable to fire than brick or stone.

- Water damage: Timber can be more susceptible to rot or swelling if moisture enters the frame.

- Rebuild cost: Specialist contractors and materials are often required for repairs, which can increase claims costs.

- Age and design: Modern engineered timber is generally more resilient than older frames, but insurers will still ask about construction type, maintenance, and any fire prevention measures.

None of this means timber homes are uninsurable. It just highlights why insurance comparison sites often fall short for owners of timber frame homes.

Why Comparison Sites Are Not The Best Option

Comparison websites are designed for standard properties. Many don't differentiate between timber and brick construction or offer the option to declare non-standard materials accurately. What's more, selecting the wrong description on a price comparison site could lead to an invalid policy or rejected claims.

Homeowners who rely solely on automated comparison quotes may find their chosen insurer later declines cover once the true construction gets disclosed. A tailored quote from a specialist broker ensures the property is assessed correctly and that cover terms are appropriate for the materials and rebuild costs involved.

How To Find The Right Insurance For Timber Framed Houses

To obtain the best insurance for timber-framed houses, homeowners should:

- Provide full construction details, including the type of frame and wall cladding.

- Confirm fire protection features such as alarms and suppression systems.

- Keep maintenance records to demonstrate responsible ownership.

- Work with a broker who understands non-standard construction and has access to specialist insurers.

Get Specialist Timber Framed House Insurance With Crowthorne

Owning a timber frame home shouldn't mean overpaying for protection. At Crowthorne Insurance, we arrange competitive, reliable timber-framed house insurance policies designed to reflect the property’s true risk profile. As members of the British Insurance Brokers’ Association (BIBA), we provide expert, impartial advice with access to leading specialist insurers.

Avoid the frustration of comparison sites. Contact Crowthorne today for expert guidance and a personalised quote on insurance for timber-framed houses.

Image Source: Canva

Why The Construction Method Of Your Timber Frame House Matters To Insurers?

Timber Framed House Insurance: Common Pitfalls and How to Avoid Underinsurance

No Comments Yet

Let us know what you think