By Crowthorne Insurance on Apr 16, 2026 11:00:00 AM

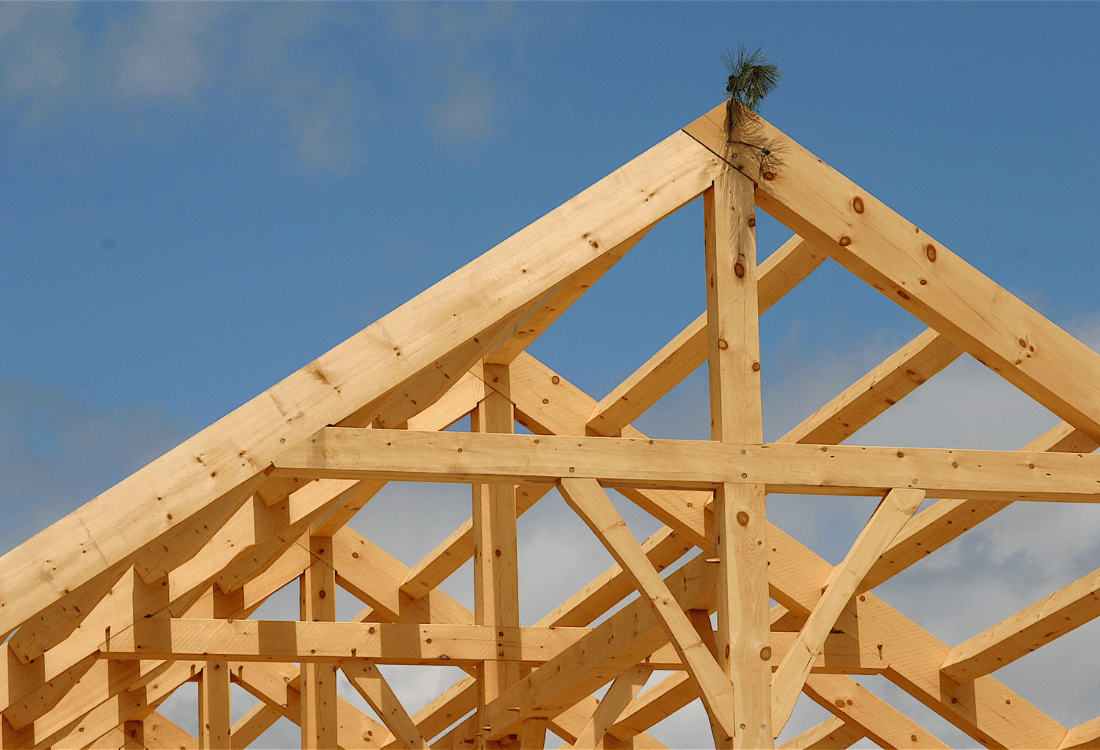

Timber frame construction is a popular and well-established building method in the UK, used in over 20% of British homes. Despite its many advantages, insurers often treat timber frame properties as non-standard risks when compared to traditional brick-and-mortar construction.

Understanding why this happens is essential when arranging appropriate cover.

This article explains why insurers scrutinise the construction of timber frame houses, the technical concerns behind this approach, and how specialist advice can help homeowners get the protection they need.

Why Timber Frame Homes are Classed as Non-Standard?

Most insurers categorise properties based on construction type. Homes built with brick or stone walls and tile or slate roofs are typically considered standard. Timber frame properties fall outside this definition, which is why, when it comes to home insurance, timber-framed houses are often treated differently.

This does not mean your timber-framed house is unsafe or high-risk. It just means that insurers recognise that different materials behave differently under stress or prolonged exposure to moisture.

These differences affect the potential cost of repairs. As a result, some insurers apply stricter underwriting criteria or avoid timber frame risks altogether.

Fire Risk and Insurer Concerns

One of the primary reasons insurers scrutinise the construction of timber frame houses is fire behaviour. Timber is combustible, and although modern fire-resistant treatments and building regulations significantly reduce risk, insurers still assess the potential for faster fire spread compared to metal or masonry structures.

Therefore, insurers focus on fire detection systems, compartmentalisation, and overall build quality when assessing timber-framed houses' insurance policies.

Moisture and Hidden Structural Risks

Another key consideration is moisture management. Timber frame structures rely on effective weatherproofing and ventilation to remain sound. If moisture permeates the structure, without early detection, it may lead to hidden decay, mould, or eventual structural damage.

Because timber framing is often concealed behind external cladding or brick skins, problems may not be visible. This potential for concealed damage is one reason insurers assess home insurance timber-framed houses more carefully than standard builds.

Proper maintenance, drainage, and ventilation systems significantly reduce this risk, but insurers need reassurance that these measures are in place and maintained correctly.

Why Automated Systems Often Reject Timber Frame Homes?

Many insurers rely on automated underwriting systems designed primarily around standard property types. These systems struggle to account for the nuances of non-standard construction.

As a result, homeowners seeking timber-framed houses insurance through comparison sites may experience automatic declines or unsuitable policy offers. The system doesn't necessarily reject the property based on actual risk, but because it does not fit a set of criteria.

This can leave homeowners with the false impression that their property is difficult or expensive to insure. The truth is that it simply needs to be assessed properly.

The Importance of Accurate Representation

Accurate disclosure of construction details is essential when arranging home insurance for timber-framed houses. Insurers need clear information about the frame type, external finishes, fire protection measures, and maintenance history.

Incomplete or unclear information can lead to inappropriate policy terms, exclusions, or declined claims. This is particularly important for timber frame homes, where small details can significantly influence underwriting decisions.

How Specialist Brokers Add Value?

This is where specialist brokers play a crucial role. Brokers who understand timber frame construction also understand how insurers assess these properties and which underwriters are comfortable covering them.

Rather than submitting your details to an automated system, a specialist broker presents your home to underwriters in context. They provide detailed information to demonstrate how the property is built, how risks are mitigated, and why it is a suitable risk for insurance.

Avoiding Gaps In Cover

One of the biggest risks for timber frame homeowners is assuming that any policy offering cover is suitable. Some policies may technically insure the property but include exclusions or limits that undermine protection.

A broker-led approach ensures policy wording, rebuild values, and exclusions align with the specific characteristics of your home. This reduces the risk of underinsurance or claim disputes.

Confidence Through Proper Protection

Timber frame homes are durable, efficient, and increasingly popular. The key to insuring them successfully lies in understanding how insurers assess risk and ensuring your property is presented accurately.

With the right support, insurance can be arranged on sensible terms that reflect real-world risk rather than automated assumptions.

Need Specialist Advice For Your Timber Frame Home?

The construction of timber frame houses matters to insurers because it affects how risks are evaluated, not because these homes are inherently unsafe. By getting to know these concerns and working with specialists who understand timber frame construction, homeowners can secure reliable, appropriate cover.

Choosing expert advice helps ensure your home’s unique structure is protected properly, providing confidence that your insurance will perform when it matters most.

If your home is timber-framed and you want insurance that reflects how it is actually built, request a callback to speak to a specialist who understands non-standard construction.

Image Source: Envato

Timber Framed House Insurance: Common Pitfalls and How to Avoid Underinsurance

Are Timber Frame Houses More Expensive To Insure?

No Comments Yet

Let us know what you think