By Crowthorne Insurance on Dec 23, 2025 10:00:01 AM

Not every home fits neatly into the criteria used by standard insurers. From unique builds to properties with a history of flooding or recent renovations, some homes require more tailored protection. If your property has distinctive features or an unusual history, you may need a non-standard build home insurance policy to ensure full cover.

This guide explains what qualifies as a non-standard property, the factors insurers look at, and how to find the right protection for your home.

What Is A Non-Standard Home Insurance Policy?

Non-standard home insurance policies are designed for properties that don’t conform to conventional building methods or risk profiles.

Most standard policies assume a home is built from brick or stone with a pitched and tiled roof, no structural issues, and no significant alterations.

If your home differs from that in materials, layout, or history, insurers may classify it as non-standard.

This doesn't mean you'll be excluded from cover altogether. You’ll simply need a specialist policy that reflects those differences.

Types Of Properties That May Need Non-Standard Cover

According to leading UK insurers and brokers, you may need insurance for non-standard construction homes if your property falls into one of the following categories:

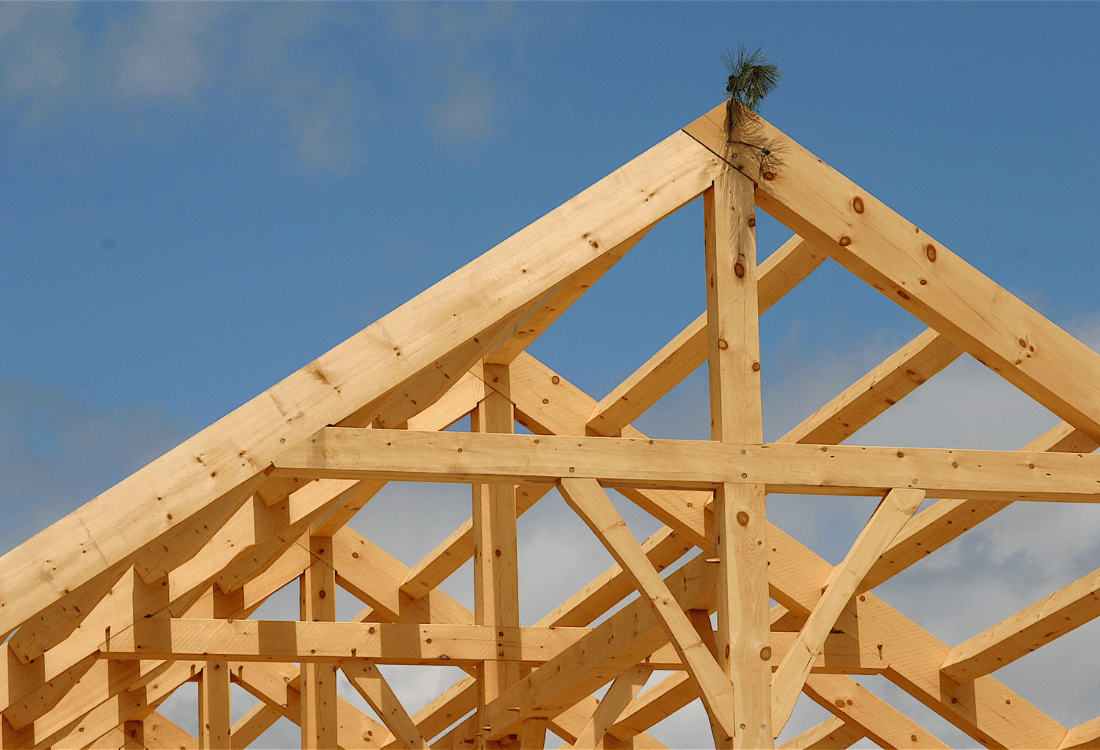

- Unusual construction materials: Homes built with timber frames, steel, glass, cob, thatch, or concrete panels.

- Listed buildings: Protected properties that require specialist repair methods and materials.

- Properties with a history of flooding or subsidence: Even if repairs have been completed, past incidents can increase risk profiles.

- Converted or extended homes: Including barn, church, or loft conversions and major structural renovations.

- Homes with flat or green roofs: These can raise the likelihood of water damage or structural stress.

- Mixed-use properties: Homes that also serve as business premises.

If your home fits any of these descriptions, a standard insurer may not provide full cover, or exclusions may apply.

What Insurers Assess When Classifying A Property

When determining eligibility for standard or non-standard insurance, underwriters look at several factors:

- The age and construction of the property

- The materials used for walls and roof

- The condition and maintenance of the building

- The location and environmental risk, including flood zones or subsidence areas

- The property’s use, including whether it’s occupied year-round or used for business

Each of these factors affects rebuild costs and claim likelihood, which is why accurate disclosure is crucial.

Why Full Disclosure Matters

If you fail to tell your insurer about unique features, previous damage, or construction details, your policy could be invalidated, leaving you liable for repair costs.

Always confirm the materials used in your home’s construction and declare any major renovations, listed status, or previous insurance refusals. Being transparent allows your insurer to provide the right level of cover from the start.

Finding The Right Cover For Your Property

If your home doesn’t qualify for standard insurance, don’t worry. You still have options. Specialist brokers can access insurers that understand non-standard risks and can build policies tailored to your property’s design, materials, and history.

At Crowthorne Insurance, we help homeowners find the right insurance for non-standard construction homes, ensuring their properties are properly protected. As proud members of the British Insurance Brokers’ Association (BIBA), we work with trusted insurers offering fair, flexible terms for non-standard homes. Protect your unique property with confidence. Contact Crowthorne today for expert advice and a personalised quote on non-standard home insurance policies.

Image Source: Canva

Flood Zones and Insurance: What Homeowners Need To Know?

Are Timber Frame Houses More Expensive To Insure?

No Comments Yet

Let us know what you think